Published On Sep 14, 2016

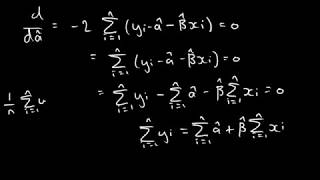

We consider the properties of the OLS/method of moments (MM) estimator in the linear regression model for stationary time series.

We show that the estimator is unbiased and consistent, and we illustrate asymptotic normality of the estimator.

show more